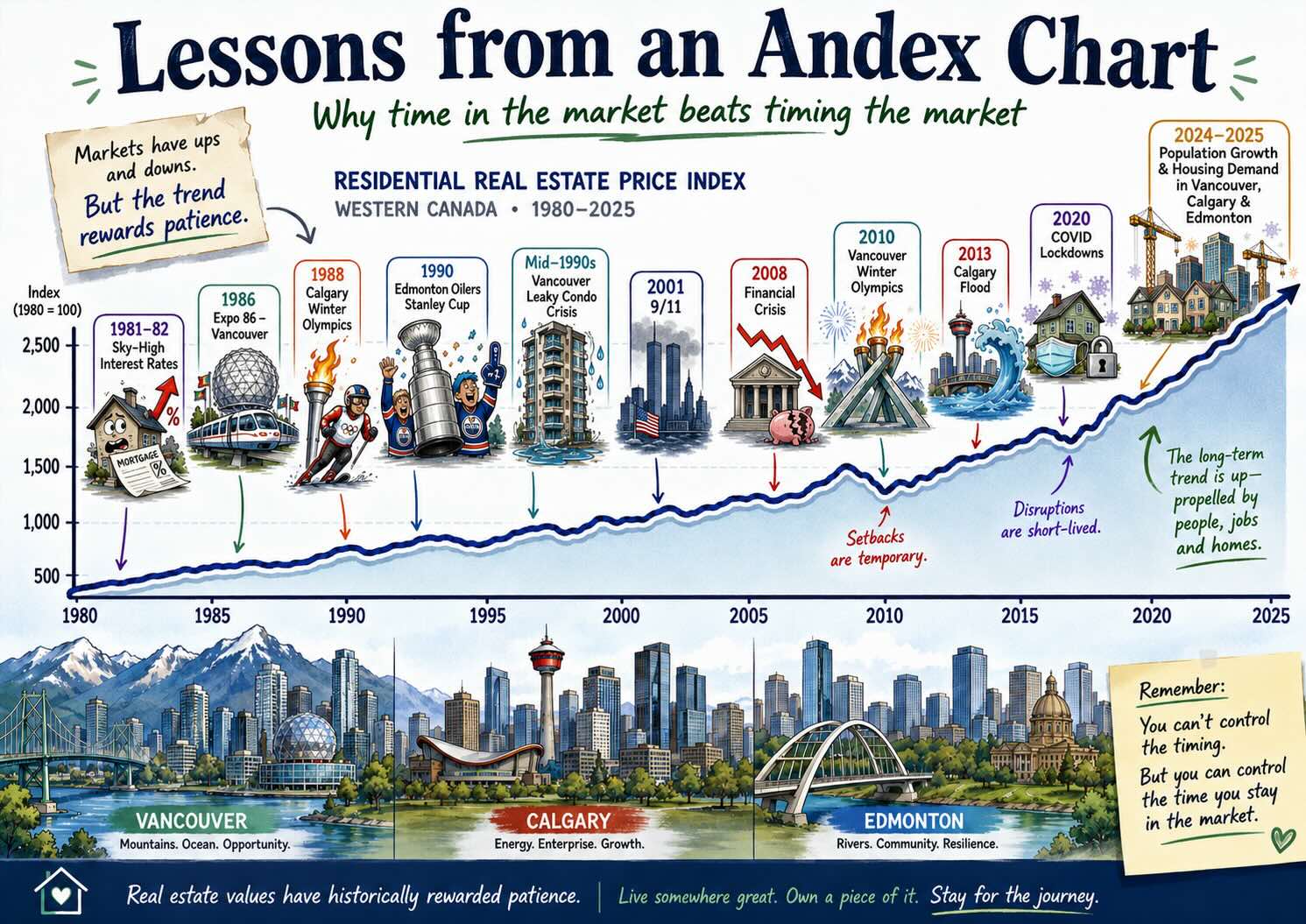

Vancouver, Calgary, Edmonton, the Interior, the Island — they're all in different places in the real estate cycle right now. But there's one truth that applies ...

Mortgage qualification can feel like being put on trial. From income documents to down payment paper trails, lenders are asking more questions than many ...

Canada’s mortgage market is changing beneath the surface. Some financing options are opening up, while others are becoming harder to access. Here’s what ...

Divorce is emotional — but mortgage qualification is mathematical. In this article, Marko Gelo explains three major mortgage problems that separating couples ...

Mortgage rates appear steady, but inflation pressure, oil volatility, and global uncertainty are quietly building. This post explains what’s really ...

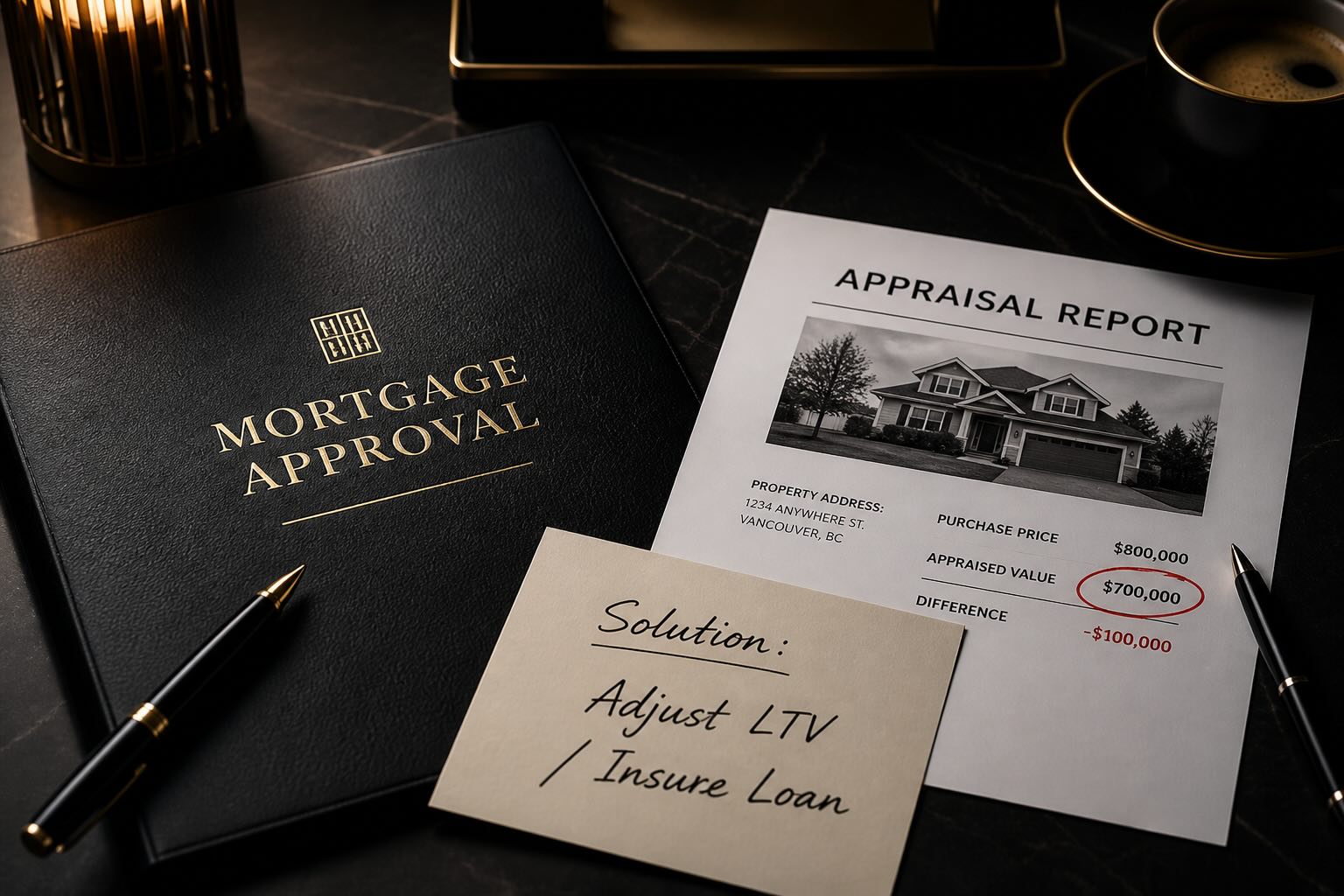

What happens when an appraisal comes in low? Learn how mortgage structure, insured financing, and lender strategy can help keep your deal alive.

March 7, 2026 The Quiet Shift Happening Inside Canadian Homes And Why It May Be the Most Underrated Real Estate Strategy in Vancouver & Calgary ...

November 17, 2025 On November 12, the Bank of Canada released its Third Quarter Financial Report. I don’t usually pay much attention to these releases, but I ...

Oct 20, 2025 Let’s call it like it is — owning a home in Canada has become unattainable for the average person. Whether you’re a first-time buyer, a young ...

August 15, 2025 This article aims to clarify the one-time closing costs incurred during real estate transactions and their role in your overall ...

Updated Post: August 30, 2025 Original Post: August 2, 2025 Canada is in the midst of an unprecedented intergenerational wealth transfer — an estimated ...

June 27, 2025 Owning a home is a dream for many Canadians, but rising costs have made it increasingly challenging, especially for first-time home buyers. On ...

- 1

- 2

- 3

- …

- 8

- Next Page »