Markets are pricing just a 9% chance of a rate cut at next week's Bank of Canada meeting — but a 53% chance of a hike by December. That flip quietly rewrites ...

The Bank of Canada held at 2.25% — but markets are pricing a hike by December. Here's what Macklem said, what he didn't, and how to choose your term.

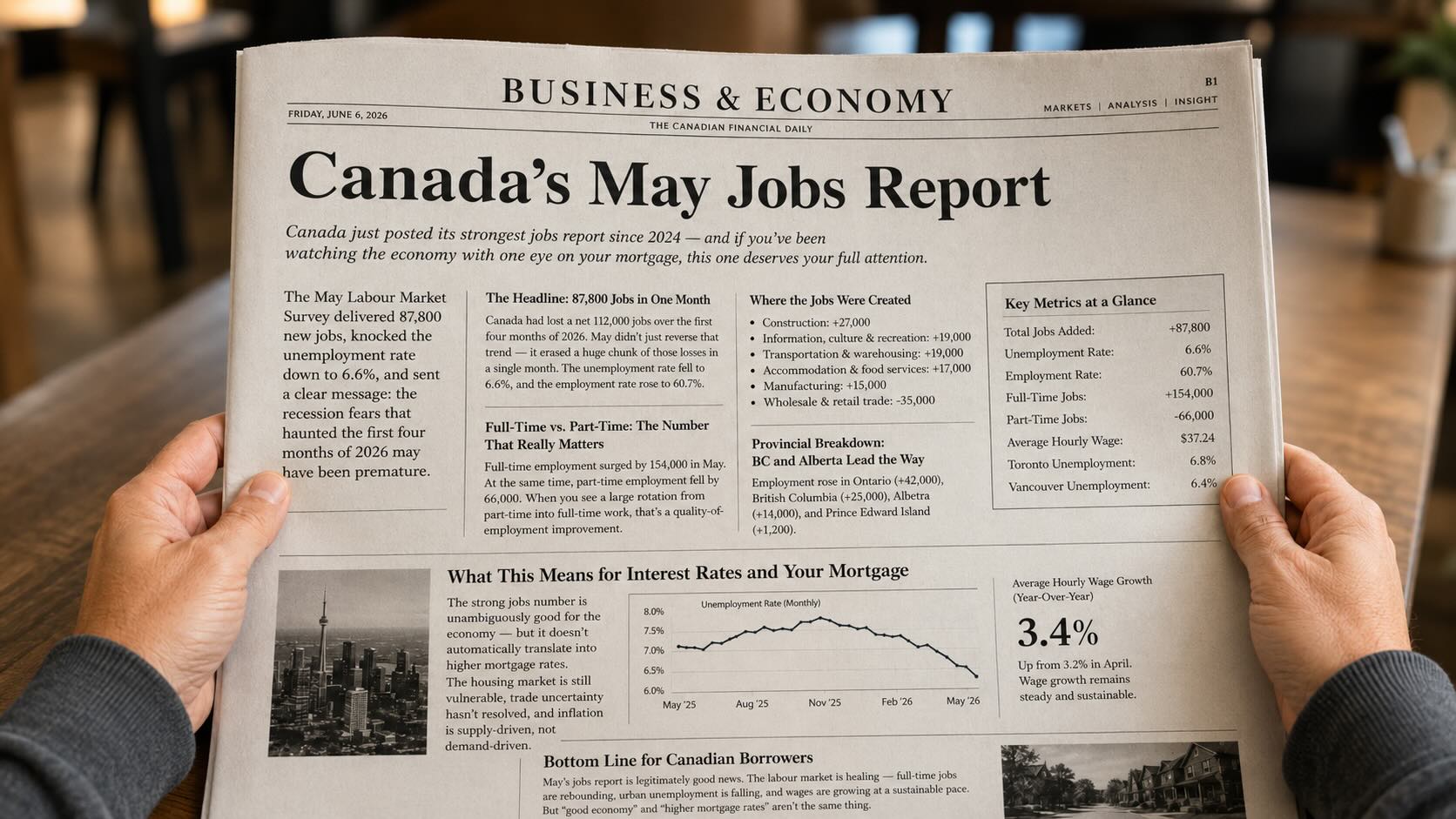

Canada added 87,800 jobs in May — the strongest gain since 2024. Here's what it means for interest rates, housing, and your mortgage.

A Middle East flare-up sent oil prices soaring this week — and Canadian mortgage rates felt it. Here's what it means for your renewal or purchase.

Canada’s latest GDP report showed weakness, including a sharp drop in residential investment. But with April showing signs of strength, rate cuts are not ...

March 18, 2026 Bank of Canada Rate Announcement: What It Means for Mortgage Rates The Bank of Canada has held its policy rate at 2.25%, keeping most bank ...

March 18, 2026 I recently read an economic report from Rennie Intelligence that highlighted just how sharply population trends have shifted across Metro ...

Feb 2, 2026 So here we are, with January 2026 firmly behind us—and what a month it was! …Okay, I’m exaggerating. It was actually pretty uneventful. Canada’s ...

Jan 4, 2026 As we progress into 2026, Canada’s housing markets continue to evolve — and not all regions are moving in the same direction. Local market ...

December 5, 2025 The interest rate environment continues to be dynamic, unpredictable, and highly influenced by global forces rather than domestic ...

November 17, 2025 On November 12, the Bank of Canada released its Third Quarter Financial Report. I don’t usually pay much attention to these releases, but I ...

Oct 13, 2025 With interest rates beginning to ease from recent highs and several positive indicators emerging, there’s reason for cautious optimism. Let’s ...