Updated Post: August 30, 2025

Original Post: August 2, 2025

Canada is in the midst of an unprecedented intergenerational wealth transfer — an estimated $1–2 trillion is expected to move from baby boomers (born 1945–1965) to their millennial and Generation X children between 2023 and 2026. While we often think of a wealth transfer as a full inheritance passed down after death, what is unfolding in many Canadian families looks a little different.

Rather than gifting entire properties outright, many parents and grandparents are selling to their children or grandchildren at discounted prices. The arrangement keeps ownership within the family, but still allows the older generation to access some of the property’s value (while they are still alive) — an important consideration as they fund retirement, healthcare, or simply maintain lifestyle security. In this sense, it’s less like a full inheritance and more like an early handoff at a discount — a bridge between gifting and selling at full market value.

These transactions, commonly referred to as Gifted Equity Purchases, allow younger buyers to enter the housing market with little or no cash out-of-pocket. The down payment is carved out of the existing equity rather than from traditional savings, enabling the transfer of wealth in a way that balances both generations’ needs: preserving financial independence for the parent, while creating an attainable path to homeownership for the child.

What is a Gifted Equity purchase?

Private home sales between family members — commonly referred to as Gifted Equity Purchases — have become increasingly common in Canada over the past several years. These arrangements typically involve one family member selling a property to another at fair market value, while also gifting the buyer the required down payment.

In effect, the down payment comes directly from the existing equity in the home, allowing the buyer to complete the purchase with no cash out-of-pocket. Essentially, the elder family member is not quite giving away the entire property, but they are providing a substantial boost by embedding the down payment into the transaction so the buyer can qualify for the mortgage.

Why mortgage guidance is critical?

If the transaction doesn’t involve a mortgage, the process is usually straightforward — a lawyer can update the land title to reflect the change in ownership. But once mortgage financing enters the equation, the complexity increases.

Gifted Equity Purchases introduce extra steps above and beyond a standard home purchase. The lender and insurer will require the purchase agreement and supporting documents to be worded in very specific ways, and the gifted equity must be clearly identified and traceable back to the home’s equity. A small misstep in the paperwork can delay or even derail the mortgage approval.

That’s why it’s critical to involve an experienced mortgage broker from the very beginning. Unlike a realtor or lawyer who may focus solely on the purchase contract or title transfer, a mortgage broker quarterbacks the entire process with the lender’s qualification rules in mind. A seasoned broker will:

- Confirm the deal structure qualifies before the contract is drafted.

- Provide ready-to-use templates tailored for Gifted Equity Purchases.

- Coordinate with lawyers to ensure the documentation matches lender requirements.

- Flag potential issues early so the mortgage funds smoothly at closing.

In short, the broker ensures that what looks like a “simple family deal” on the surface actually meets the stricter demands of Canada’s mortgage system.

Step-by-Step Guide to a Compliant Gifted Equity Purchase

1. Negotiate the Purchase Price

Agree on a fair market value purchase price with the current owner (the family member selling the property).

2. Engage a Mortgage Broker First

When a mortgage is required, the most important factor is meeting the lender’s qualification criteria — not just drafting a contract. That’s why a mortgage broker experienced in Gifted Equity Purchases should be your first point of contact.

Unlike a realtor who may charge a fee to draft the purchase agreement, or a lawyer who will likely increase their standard fee to quarterback the process, a mortgage broker offers end-to-end guidance at no additional cost to you — they’re compensated directly by the lender.

A qualified broker understands the nuances of these transactions and can ensure the purchase contract and gifted equity documentation are structured to meet lender and insurer requirements. They often provide ready-to-use templates, coordinate with the legal team, and ensure nothing is missed that could derail the deal at the funding stage.

3. Draft the Gifted Equity Purchase Contract

Once the broker has confirmed the qualification strategy, the purchase agreement can be prepared — with clear wording identifying the gifted down payment and its origin from the home’s equity.

4. Proceed with Mortgage Qualification

The mortgage approval process generally mirrors a traditional purchase, except the down payment isn’t from the buyer’s savings — it’s built into the equity. When properly structured, this results in a $0 out-of-pocket purchase for the buyer, while satisfying all lender and insurer criteria.

Example Scenario

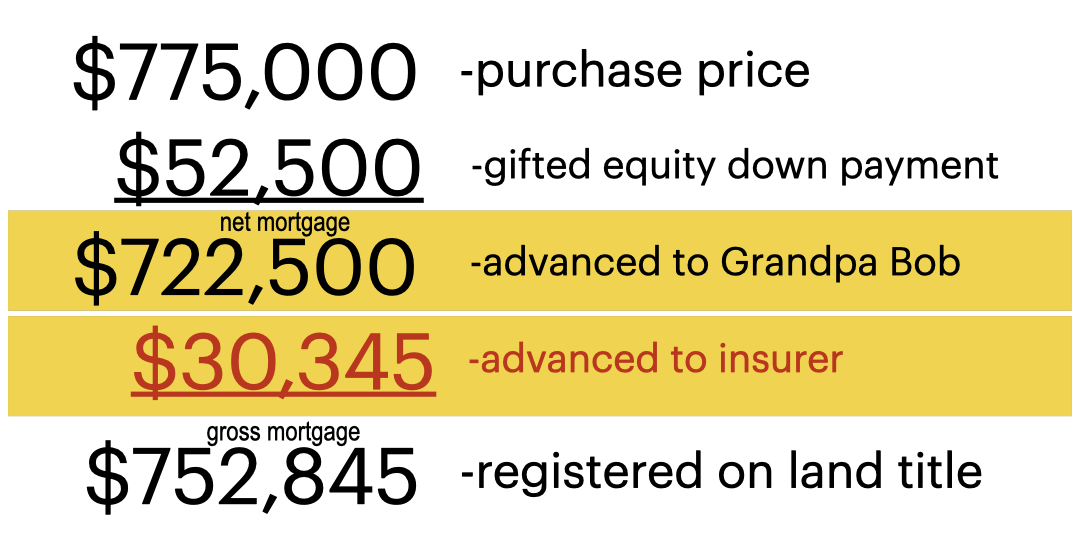

Bob owns a property with a fair market value of $800,000. He plans to move into a senior care facility and wants to help his grandson, Jimmy, become a homeowner. They agree on a sale price of $775,000. Jimmy requires a mortgage to buy the property.

To assist, Bob not only sells the property below market value but also gifts the required down payment. Normally, a minimum of $52,500 is needed for a purchase at this price point (5% on the first $500,000 and 10% on the remaining $275,000). Rather than gifting cash, Bob allocates a portion of the home’s equity as the down payment. In effect, Jimmy never receives physical funds — the down payment is embedded in the transaction, enabling Jimmy to qualify for a mortgage with $0 out of pocket.

Gifted Equity Purchases offer a creative and compassionate way for families to transition property ownership and support younger generations in entering the housing market. But they are not standard purchases — they come with unique requirements that demand careful structuring and lender-approved documentation.

An experienced mortgage broker is the key player in making these transactions successful. With the right guidance, families can avoid unnecessary delays, meet all lender and insurer requirements, and ensure the wealth transfer takes place smoothly. If you’re considering this route, seek professional advice early to protect both generations’ interests and to ensure the transaction fulfills its intended purpose: keeping wealth in the family while opening doors to homeownership.

Are you considering a Gifted Equity Purchase? Link up directly with Marko for more information (see below, “Connect With Marko”).

Call Marko Gelo at 604-800-9593 for his expert mortgage advice.

Download my amazing Mortgage App…it’s loaded with calculators and tons of useful information!

Don’t want to miss out on the next blog post? Click Here to have future issues emailed directly to your inbox!

CONNECT WITH MARKO:

604-800-9593 cell/text | 403-606-3751 cell/text | Schedule A Call | WhatsApp | Marko’s App | mortgages@markogelo.ca