Topics associated with various forms of down payment.

Down Payment

0

0

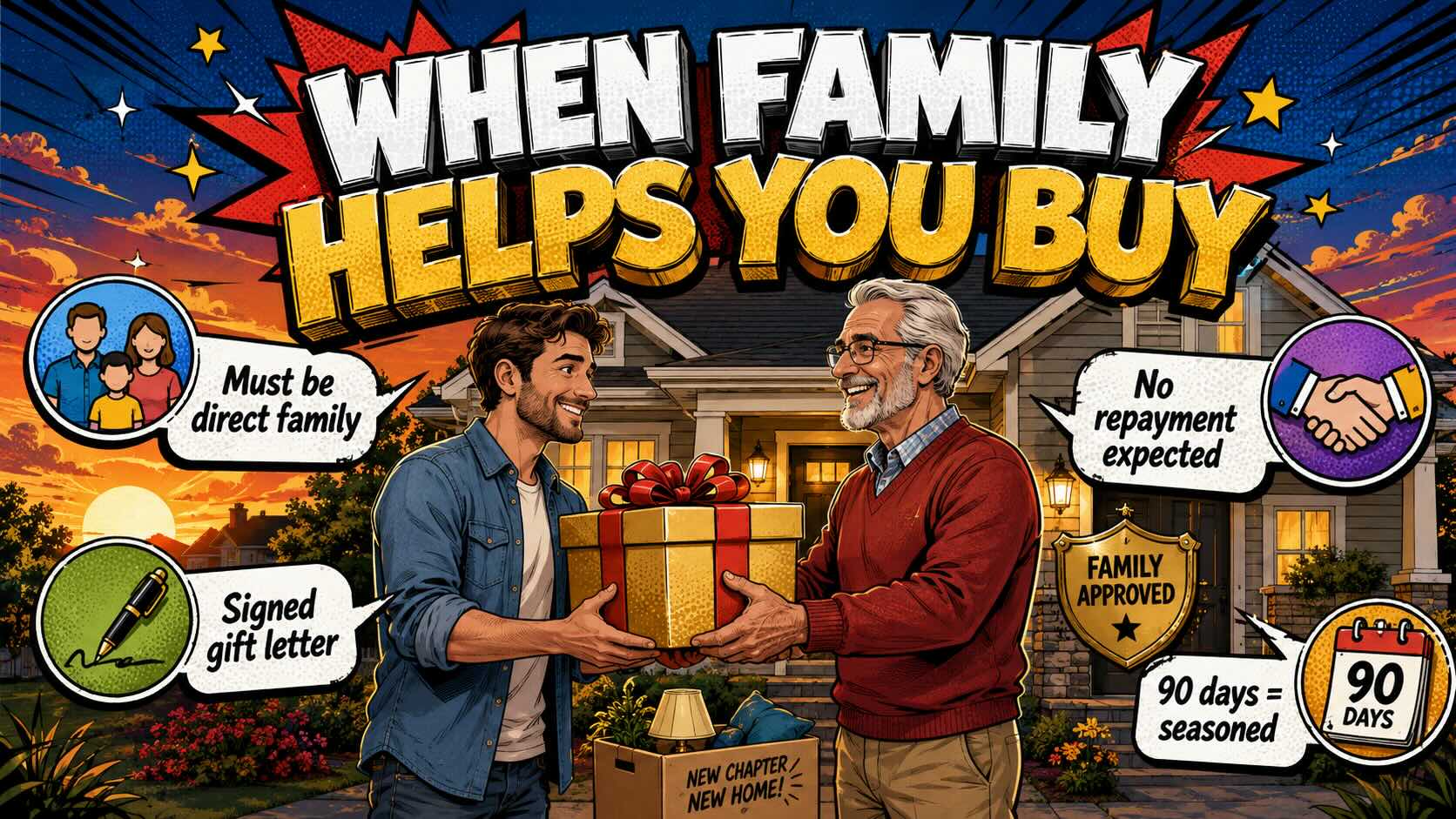

If family is helping with your down payment, timing matters more than you'd think. Most people don't know that gifted funds sitting untouched in your account ...

0

-1

August 15, 2025 This article aims to clarify the one-time closing costs incurred during real estate transactions and their role in your overall ...

0

0

(October 5, 2024) On August 1, 2024, the Government of Canada implemented significant reforms to its mortgage qualification process to help more Canadians, ...

0

0

(September 21, 2024) Financial crimes have long been entrenched in Canada's real estate and banking ecosystem, creating a deeply embedded problem that cannot ...

0

0

(February 18, 2024) Don't want to miss out on the next blog post? Click Here to have future issues emailed directly to your inbox! Securing a ...

0

0

(Sept 30, 2023) Don't want to miss out on the next blog post? Click Here to have future issues emailed directly to your inbox! Embarking on a career ...

0

0

Mortgage Programs in Canada for Doctors who are in the process of or completing residency/fellowship

(Sept 25, 2023) Don't want to miss out on the next blog post? Click Here to have future issues emailed directly to your inbox! In Canada, the journey ...

0

0

(Sept 22, 2023) Don't want to miss out on the next blog post? Click Here to have future issues emailed directly to your inbox! When qualifying for a ...