September 3, 2025

Once hailed as a safeguard against reckless borrowing, the Canadian mortgage stress test has quietly shifted into the background of our housing conversation — not gone, but no longer the headline shock it was when first introduced in 2016. Today, it’s become one of those “can’t live with it, can’t live without it” policies. On one hand, it acts as a lid on lending volumes, arguably protecting households from over-indebtedness and preserving the stability of Canada’s real estate market. On the other hand, it continues to shut out many creditworthy buyers who could comfortably manage their payments at real-world rates but are disqualified under the inflated qualifying thresholds. This tension — between prudence and exclusion — defines the stress test’s legacy and its controversial role in shaping who gets to participate in Canada’s housing market.

A Brief Recap

The mortgage stress test has been one of the most significant regulatory changes in Canadian real estate over the past decade. Designed to ensure borrowers could handle future rate increases, the test has evolved considerably since its inception in 2016.

2016 – Initial Introduction (Insured Mortgages Only)

On October 17, 2016, the federal government introduced the stress test for insured mortgages (those with less than a 20% down payment). Borrowers had to qualify at the Bank of Canada’s 5-year benchmark rate rather than their actual contract rate.

-

The benchmark rate was calculated as the average of the posted 5-year fixed rates at the Big Six banks, and it was almost always higher than actual contract rates.

-

At the time, this qualifying rate hovered in the 4.6%–5.2% range, even when borrowers were often securing rates around 2.5%.

-

The goal was to curb rising household debt and ensure affordability even if rates increased.

2018 – Expanded to All Mortgages

On January 1, 2018, OSFI (Office of the Superintendent of Financial Institutions) expanded the stress test to cover all uninsured mortgages (20%+ down). Borrowers now had to qualify at the greater of:

-

The Bank of Canada’s 5-year benchmark rate, or

-

The contract rate + 2%.

This change immediately reduced borrowing power by roughly 15–20%, pulling many buyers out of the market.

2019–2020 – Rising Criticism

As interest rates trended downward, economists and industry groups criticized the test for being too restrictive. Many argued that tying the qualifying rate to the posted 5-year benchmark created an artificial hurdle, as posted rates were much higher than real contract rates.

2020 – Proposed Adjustment (Delayed by COVID-19)

In early 2020, the Department of Finance announced plans to replace the benchmark with a more market-based calculation — the average 5-year fixed rate on new insured mortgages. This was meant to create a qualifying rate more reflective of what borrowers actually faced in the market. Implementation was delayed due to the pandemic.

2021 – Key Revision

On June 1, 2021, OSFI finally introduced the revision. The rule for both insured and uninsured mortgages became:

-

Borrowers must qualify at the greater of the contract rate + 2% or 5.25% (minimum qualifying rate).

This change decoupled the stress test from the banks’ posted rates, which were often inflated, and created a more predictable and transparent standard.

2022–Present – Higher Impact from Rising Rates

As interest rates surged through 2022 and 2023, the stress test became even more restrictive. Borrowers were often qualifying at 7–8% or higher, while actual contract rates were already 5–6%. This further reduced affordability and borrowing capacity during a period of record-high home prices.

The Stress Test Today

Fast-forward to today, and the mortgage stress test still applies to all new mortgage qualification scenarios. That includes:

-

New purchases

-

Equity take-outs or increasing your loan amount

But here’s the key: mortgage renewals are exempt.

Renewals: When the Stress Test Doesn’t Apply

Whether you stay with your current lender or switch to a new one, the stress test does not apply at renewal — as long as you’re not increasing the loan amount. In these cases, you qualify at your actual contract rate.

This exemption gives renewing borrowers more flexibility, particularly in today’s high-rate environment. Without the stress test hurdle, households can shop around for better renewal terms without worrying about reduced borrowing capacity.

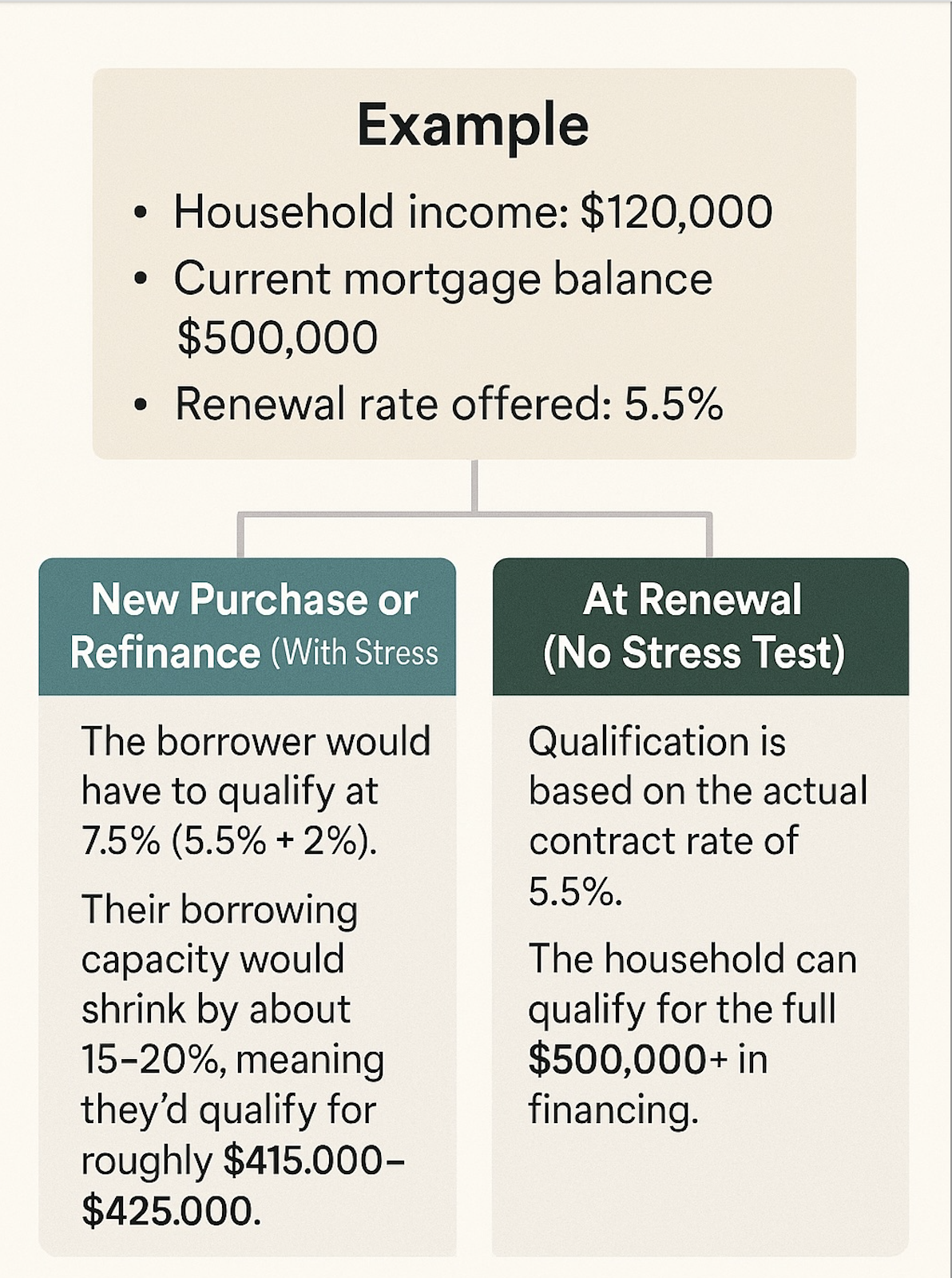

Example: How Much of a Boost Does This Make?

Let’s consider a borrower with the following profile:

-

Household income: $120,000

-

Current mortgage balance: $500,000

-

Renewal rate offered: 5.5%

If this were a new purchase or refinance (with stress test):

-

The borrower would have to qualify at 7.5% (5.5% + 2%).

-

Their borrowing capacity would shrink by about 15–20%, meaning they’d qualify for roughly $415,000–$425,000.

At renewal (no stress test):

-

Qualification is based on the actual contract rate of 5.5%.

-

The household can qualify for the full $500,000+ in financing.

That’s a boost of nearly $75,000–$85,000 in borrowing power simply because the stress test doesn’t apply at renewal.

That’s a boost of nearly $75,000–$85,000 in borrowing power simply because the stress test doesn’t apply at renewal.

Final Thoughts

Since 2016, the mortgage stress test has reshaped how Canadians qualify for mortgages. It was born out of good intentions — to safeguard households from overleveraging — but has often made affordability more difficult.

The key distinction today is this:

-

New borrowing (purchases or refinances where extra money is granted) = stress test applies.

-

Mortgage renewals (mortgage amount stays the same, doesn’t increase) = no stress test.

For homeowners facing renewal, this exemption is one of the few relief valves in Canada’s tighter lending environment. It means you can confidently explore renewal options — even with a new lender — without being held back by artificially inflated qualifying rates.

Call Marko Gelo at 604-800-9593 for his expert mortgage advice.

Download my amazing Mortgage App…it’s loaded with calculators and tons of useful information!

Don’t want to miss out on the next blog post? Click Here to have future issues emailed directly to your inbox!

CONNECT WITH MARKO:

604-800-9593 cell/text | 403-606-3751 cell/text | Schedule A Call | WhatsApp | Marko’s App | mortgages@markogelo.ca