June 3, 2026

You might be wondering what an oil tanker route in the Persian Gulf has to do with your mortgage payment in Vancouver or Calgary. The answer, as this week made clear, is: quite a lot. A series of events — a Middle East military exchange, a surprise jump in U.S. factory output, and record-setting stock markets — all landed in the same week and pushed Canadian bond yields higher. Here’s what happened, why it matters, and what you should be thinking about if a mortgage decision is on your horizon.

The Strait of Hormuz Just Became a Mortgage Story

Over the weekend, Washington struck Iranian military installations. Iran responded by targeting a U.S. base. Then Iran’s state news agency reported that Tehran had halted peace talks and threatened to completely shut down the Strait of Hormuz.

The market reacted immediately. WTI crude futures surged nearly 6% in a single session, hitting $92.16 per barrel. That kind of move matters beyond the gas pump. Oil is a major input cost throughout the economy, and when energy prices spike, inflation fears rise with them. And as Canadians who’ve lived through the last few years know very well — when inflation fears rise, central banks become reluctant to cut rates.

The U.S. Factory Data That Surprised Everyone

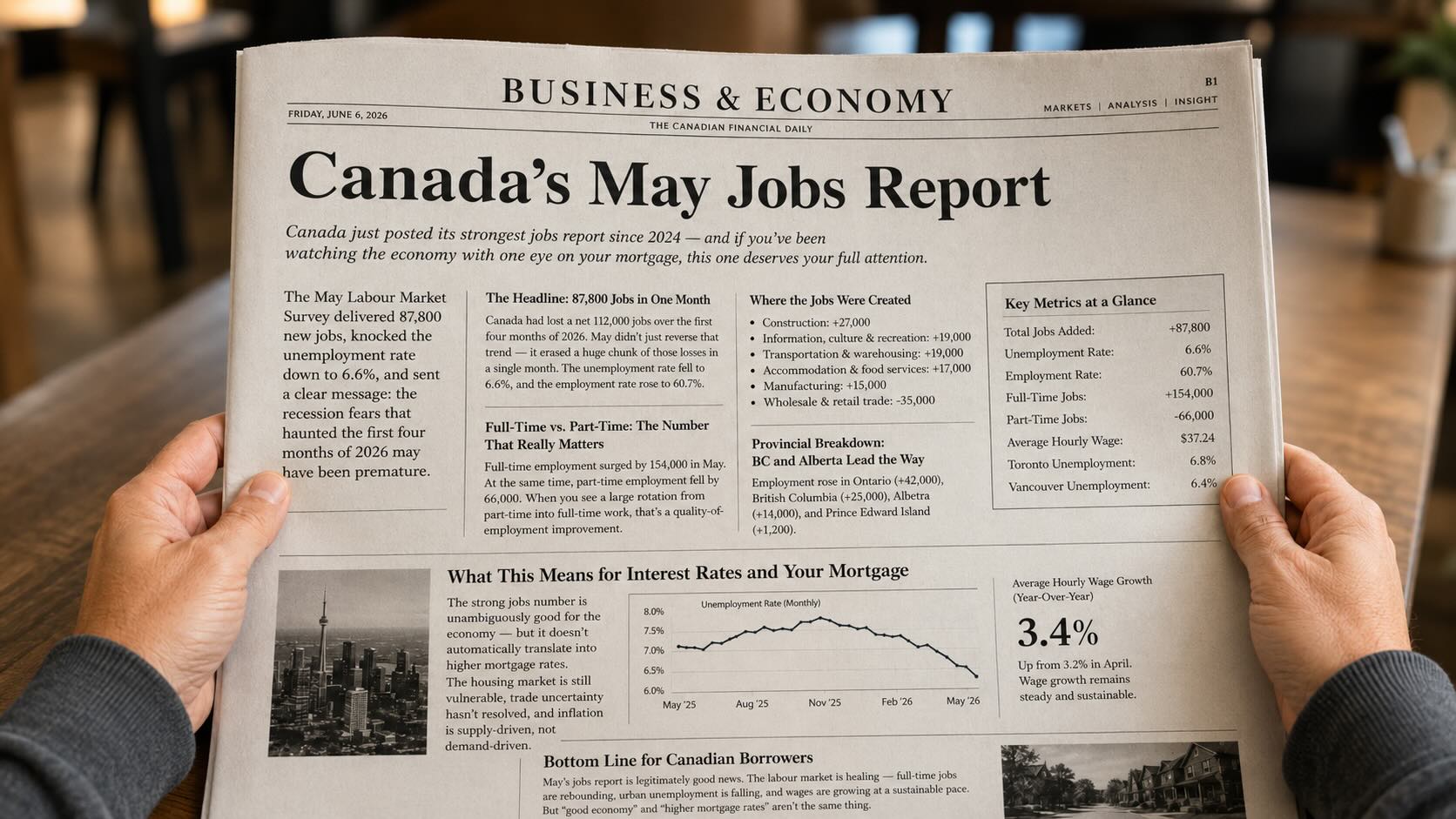

Layered on top of the oil story was a very strong ISM Manufacturing PMI out of the United States. The reading came in at 54.0 for May — ahead of the expected 53.0 and the strongest in roughly four years.

What caught the market’s attention wasn’t just the headline — it was the Prices Index, sitting at an elevated 82.1. That tells us manufacturers are still paying up for materials. It’s the kind of “hot economy” signal that makes central bankers nervous about cutting rates too quickly.

This matters to Canadian mortgage holders because U.S. and Canadian bond markets are tightly linked. When U.S. yields rise on strong economic data, Canadian yields typically follow — and fixed mortgage rates in Canada are priced off the 5-year Government of Canada bond yield. If you’re curious how the qualifying side of this works, it’s worth reading our breakdown of how the mortgage stress test factors into your qualification — because the rate environment directly affects how much you qualify for.

Where Canadian Yields Landed

| Benchmark Rate | Level | Change |

|---|---|---|

| Canada 5-Year Yield | 3.08% | ▲ 3 bps |

| U.S. 5-Year Yield | 4.17% | ▲ 2 bps |

| 4-Year Swap Rate | 2.86% | ▲ 4 bps |

| 5-Year Canada Mortgage Bond | 3.17% | ▲ 3 bps |

These moves were modest individually — but they all pointed in the same direction. The 5-year yield hit a session high before pulling back, partly due to calming words from the Bank of Canada.

The Bank of Canada’s Carefully Chosen Words

Bank of Canada Senior Deputy Governor Carolyn Rogers appeared before a House committee this week and made a notable statement: she acknowledged that two consecutive quarters of declining GDP does technically meet one definition of a recession. That’s not something central bankers say casually.

At the same time, she urged against over-weighting any single indicator — a signal that the Bank isn’t ready to declare a crisis or commit to an aggressive rate cut path. Her measured tone had a modest calming effect on Canadian yields, helping to cap the upward pressure from global events.

The Bank also provided an update on the mortgage renewal wave that dominated headlines last year. The Bank now expects this cycle to be fully absorbed by the second half of 2027. If you’re navigating a renewal right now, it’s worth understanding how the maturity and transfer process actually works — including what happens to your mortgage in the days around your maturity date and why the cost is often far lower than people expect.

Stock Markets, the AI Boom, and Yields

U.S. equity markets hit fresh record highs this week, fuelled by enthusiasm around artificial intelligence. When investors pile into stocks, money moves away from bonds — pushing bond prices down and yields up. Combined with oil and manufacturing data, that’s a three-pronged push in the same direction.

The Big Picture: What Should You Watch?

Crude oil has now bounced off the midpoint of its recent trading range five times since mid-March. Until oil decisively breaks lower and settles in the $70s, inflation risk remains an active concern for central banks — and rate cuts will come more slowly than many homeowners were hoping for earlier this year.

The path down for rates is not closed. But it is narrower and slower than it looked at the start of the year. If you have a mortgage rate hold or a purchase coming up in the next 6 to 12 months, now is the time to get organized — not to panic, but to plan.

Ready to talk about your mortgage?

I’m Marko Gelo, a dually licensed mortgage broker in BC and Alberta. Call or text me at 604-800-9593 — one application, one credit check, access to Canada’s top lenders.

Or visit homefinancingsolutions.ca to explore tools, calculators, and past episodes.

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Always consult with a qualified professional regarding your specific situation.

This article is for informational purposes only and does not constitute tax or legal advice. Always consult with a qualified professional regarding your specific situation.

Need mortgage advice in British Columbia or Alberta?

Call or text 604-800-9593 to discuss your mortgage options.

Connect with Marko

Mortgage strategy, calculators, and direct access—without the bank-branch waiting room.

604-800-9593 ph1 | 403-606-3751 ph2 | mortgages@markogelo.ca

Download the Mortgage App for calculators and planning tools, or subscribe to get future posts delivered directly to your inbox.