Since the announcement of the new mortgage rule coming in to effect on January 1, there’s been a mad rush that’s led many Canadians to push ahead with mortgage and real estate plans that were previously slated for a later date.

Here are a couple of scenarios where moving ahead with mortgage and real estate plans prior to January 1 might make sense:

- those that are anticipating (or hoping for) real estate prices to come down fear that the new mortgage rule will have a greater impact on their purchasing power than the potential savings that they would achieve by purchasing in a (hopefully) declining real estate market. The new mortgage rule is set in stone and predictable, but the real estate market is not.

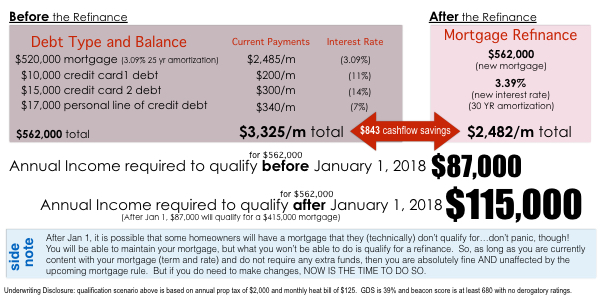

- perhaps the biggest group to be affected by the new rule change are the people who are currently contemplating whether or not to refinance or renew their mortgage ahead of its maturity. The ability to refinance (mainly to consolidate high interest debt) will severely be altered from a qualification stand point as the 2% stress test will decimate maximum borrowing amounts. For some, that might be the difference between being able to manage monthly debt loads, or not. Here is a scenario that we believe will be common:

For a refresher about the upcoming mortgage rule change, watch the video below to learn more: