November 3, 2025

Why would someone change names on a property title?

Changing who appears on your property title is one of the most significant legal and financial decisions a homeowner can make.

Whether you’re adding a spouse, removing an ex-partner, or planning your estate, understanding when and why to modify property ownership can have major implications.

Let’s examine in detail the five most common reasons that British Columbia and Alberta homeowners make these major changes.

1. Marriage or New Relationship: Adding Your Partner to Title

When should you add a spouse or partner to title?

Marriage or a long-term partnership often prompts homeowners to consider adding their partner to title. This decision blends both emotional and financial motivations — but it must be approached with full understanding of the consequences.

The Benefits of Adding a Spouse

Adding your spouse as a co-owner creates joint ownership, which offers several advantages:

- Right of Survivorship: In both B.C. and Alberta, property held as joint tenants automatically transfers to the surviving spouse upon death, avoiding probate delays.

- Shared Ownership: Joint title reflects shared commitment and simplifies decision-making over your most valuable shared asset.

Tax & Legal Considerations

Each province treats title transfers differently:

- British Columbia: Adding a spouse to title is typically exempt from Property Transfer Tax (PTT) when no money changes hands, provided the property remains a principal residence.

- Alberta: There’s no land transfer tax. Instead, there are modest/miscellaneous land title and mortgage registration fees, which are minimal compared to Ontario or B.C. Click Here for a complete list of Alberta’s Land Title and Survey fee schedule.

If the property is a rental or secondary home, the Canada Revenue Agency (CRA) may treat adding someone to title as a disposition of interest — potentially triggering capital gains tax on the transferred portion.

Matrimonial Home Rights

Both provinces extend rights to married spouses regarding the family home:

- In B.C., under the Family Law Act, both spouses share equal rights to family property and its division upon separation, regardless of whose name appears on title.

- In Alberta, the Matrimonial Property Act provides similar protection for married spouses and long-term adult interdependent partners.

Adding a spouse to title formalizes ownership but doesn’t necessarily increase their legal right to occupy the home — those rights already exist under family law.

2. Divorce or Separation: Removing Your Ex from Title

Separation or divorce is one of the most common reasons homeowners remove a name from title.

The Legal Process

You can’t unilaterally remove someone from title without their consent or a court order. The change must be supported by a written separation agreement or divorce judgment.

Typically, one spouse buys out the other’s share, arranges new financing if needed, and the transfer is registered through a lawyer or notary.

Tax & Cost Implications

- In B.C., transfers between spouses or former spouses made under a separation agreement or court order are exempt from Property Transfer Tax.

- In Alberta, because there is no provincial land transfer tax, only minor registration fees apply.

If refinancing is involved, you may need lender consent, new mortgage registration, and possibly incur penalties or legal fees.

What if your ex won’t cooperate?

If a former partner refuses to sign off despite a valid agreement or court order, you’ll likely need court enforcement. Always work through an experienced family and real estate lawyer to avoid unintended consequences.

3. Estate Planning: Adding Children or Family Members

Many parents in B.C. and Alberta consider adding adult children to title as part of estate planning — usually to avoid probate or simplify inheritance.

Why Parents Consider It

In B.C., probate fees are roughly 1.4% of the estate’s value. Adding children as joint tenants with right of survivorship means the property passes directly to them upon death, bypassing probate.

Alberta’s probate process is also relatively efficient, but some parents still attempt to avoid it for simplicity.

The Hidden Dangers

This seemingly simple move comes with serious risks:

- Exposure to Your Child’s Creditors: If your child faces debt, divorce, or legal issues, your home can become vulnerable.

- Immediate Capital Gains: Adding a child creates a disposition of that share, which can trigger capital gains tax on that portion — even if no money changes hands.

- Loss of Control: Once your child is on title, you can’t sell or refinance without their consent.

Better Estate Planning Alternatives

In both provinces, most estate lawyers discourage adding children to title. Better options include:

- Naming beneficiaries through your will,

- Using a trust to hold property, or

- Adding a registered life estate (in B.C.) that preserves control while designating future ownership.

Always seek professional estate planning advice before proceeding.

4. Business and Creditor Protection: Strategic Title Structuring

Business owners and professionals in both provinces often review title structure for asset protection.

Why It Matters

If you face business liability, professional claims, or debt judgments, creditors can register liens against property you own.

Title structuring may offer protection — but timing is everything. Transfers made after you become aware of risk can be overturned as fraudulent conveyances.

Strategic structuring should always be done proactively and with guidance from a lawyer familiar with B.C.’s Land Title Act or Alberta’s Land Titles Act.

5. Financing and Mortgage Considerations

Sometimes title changes happen not for personal or estate reasons, but to optimize mortgage qualification or rates.

When Adding Someone Helps

Adding a co-signer/owner (spouse, parent, or business partner) with strong income or credit can help you qualify for a mortgage that you otherwise wouldn’t. Lenders look at combined income and credit scores when assessing risk.

When Removing Someone Helps

Conversely, removing someone may improve your qualification if:

- The co-borrower has poor credit, or

- You want your spouse to qualify as a first-time home buyer on a new purchase.

How the Process Works in B.C. and Alberta

Step 1: Consult a real estate lawyer (Alberta) or real estate lawyer/notary (BC) to review implications and prepare transfer documentation.

Step 2: Obtain lender consent if a mortgage exists.

Step 3: Sign and register the Transfer of Land electronically through the provincial land titles office.

Step 4: Pay applicable fees and finalize registration (usually within a few days).

Simple transfers take 4–8 weeks. Complex cases — involving refinancing, disputes, or estate restructuring — can take longer.

Common Mistakes to Avoid

- Ignoring Tax Consequences: Even “gifted” title changes can create taxable dispositions.

- Failing to Update Your Will: Joint ownership can override your estate plan.

- Adding Children Without Advice: Creates tax exposure and loss of control.

- Not Informing Your Lender: May breach mortgage terms and force re-qualification

- No Written Agreement: Always clarify whether an added owner is contributing financially or receiving a gift.

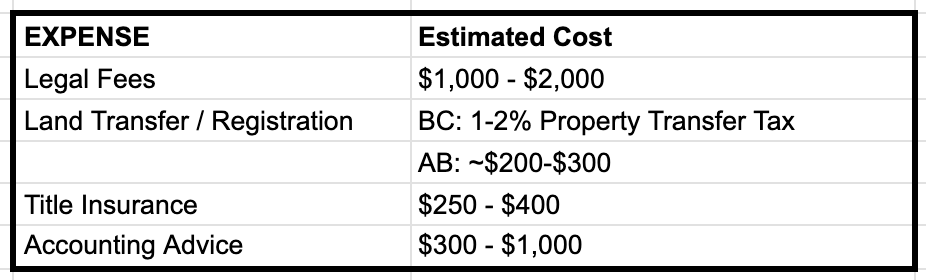

Typical Costs

Final Considerations

Before making changes to your land title, ask:

- What am I trying to achieve?

- Are there tax-efficient or safer alternatives?

- How will this affect my estate or my mortgage?

- Is everyone protected if circumstances change?

Changing title is a serious legal act. Once registered, reversing it requires cooperation from all parties and incurs similar costs again.

Seek professional guidance from a real estate lawyer and tax advisor to ensure every step is done correctly.

Disclaimer: This article is for general informational purposes only and does not constitute legal or tax advice. The information contained herein is not guaranteed to be 100% accurate or complete and is intended solely as an entry point for further understanding. Laws and regulations vary by province and individual circumstance—always verify details with a qualified accountant or real estate lawyer before proceeding.

Do you have a question about your land title? Call, text, or email Marko right now to discuss in greater detail.

RECENT BLOG POSTS:

Strategic Entry Points for First-Time Buyers in Vancouver (Oct 25, 2025)

Want to fix Canada’s Housing Crisis? Make Mortgage Payments Tax Deductible. (Oct 21, 2025)

Call Marko Gelo at 604-800-9593 for his expert mortgage advice.

Download my amazing Mortgage App…it’s loaded with calculators and tons of useful information!

Don’t want to miss out on the next blog post? Click Here to have future issues emailed directly to your inbox!

CONNECT WITH MARKO:

604-800-9593 cell/text | 403-606-3751 cell/text | Schedule A Call | WhatsApp | Marko’s App | mortgages@markogelo.ca